POLICY-DRIVEN Payment ROUTING

Your policies, applied to every payment

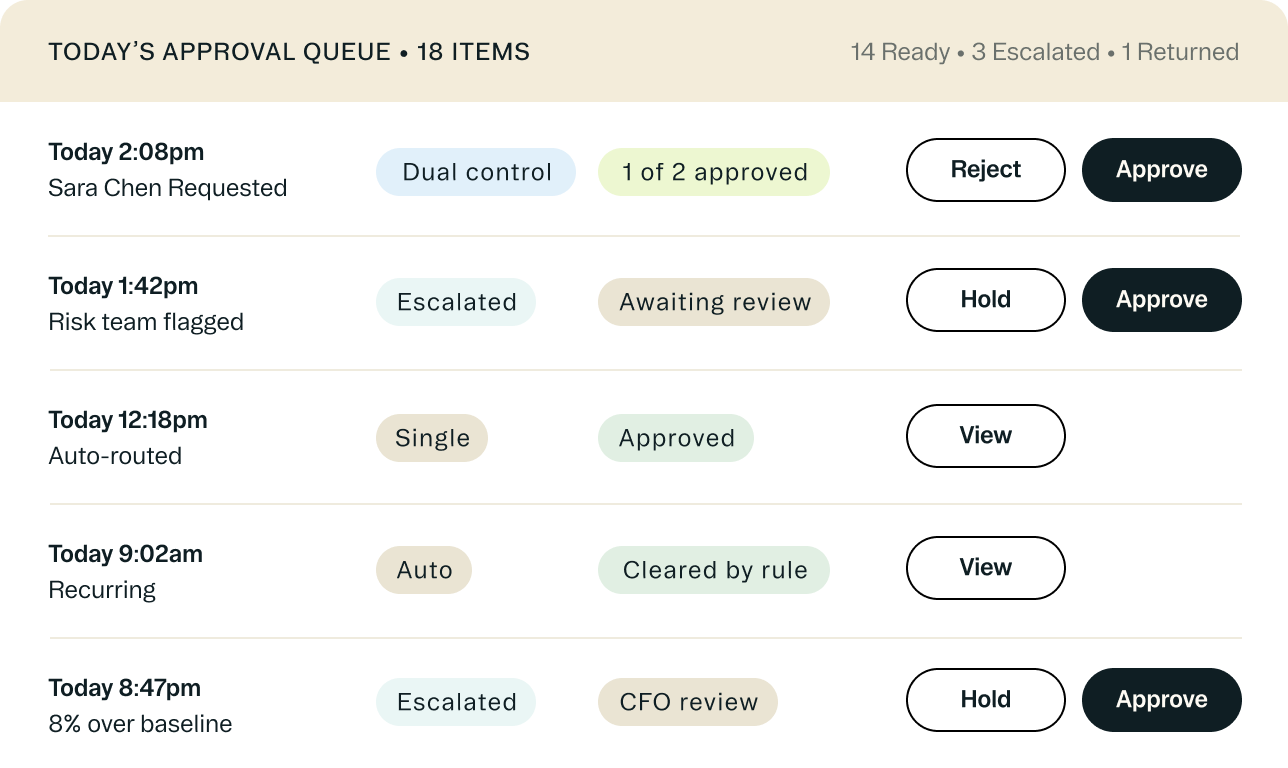

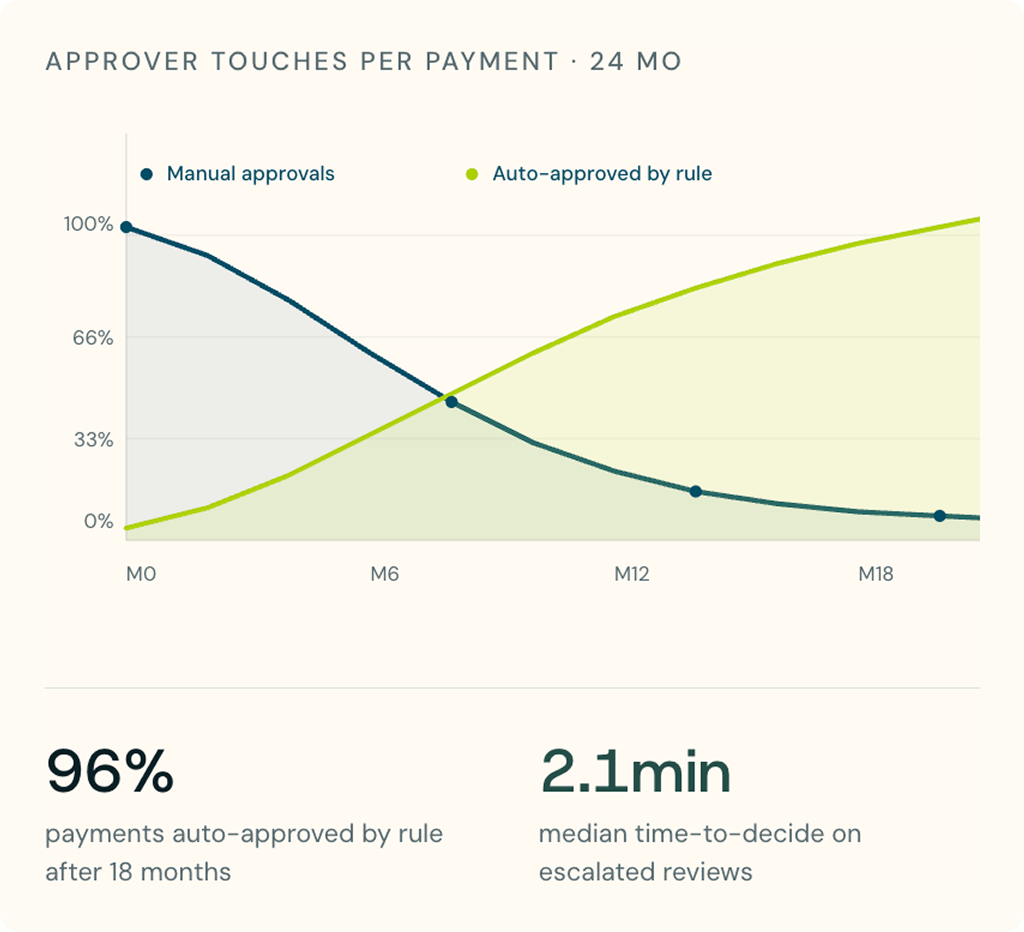

Hudson checks every payment against your rules before it moves. Routine payments clear on their own. Anything that needs a second look goes to the right approver with full context. Every decision lands in the audit trail.